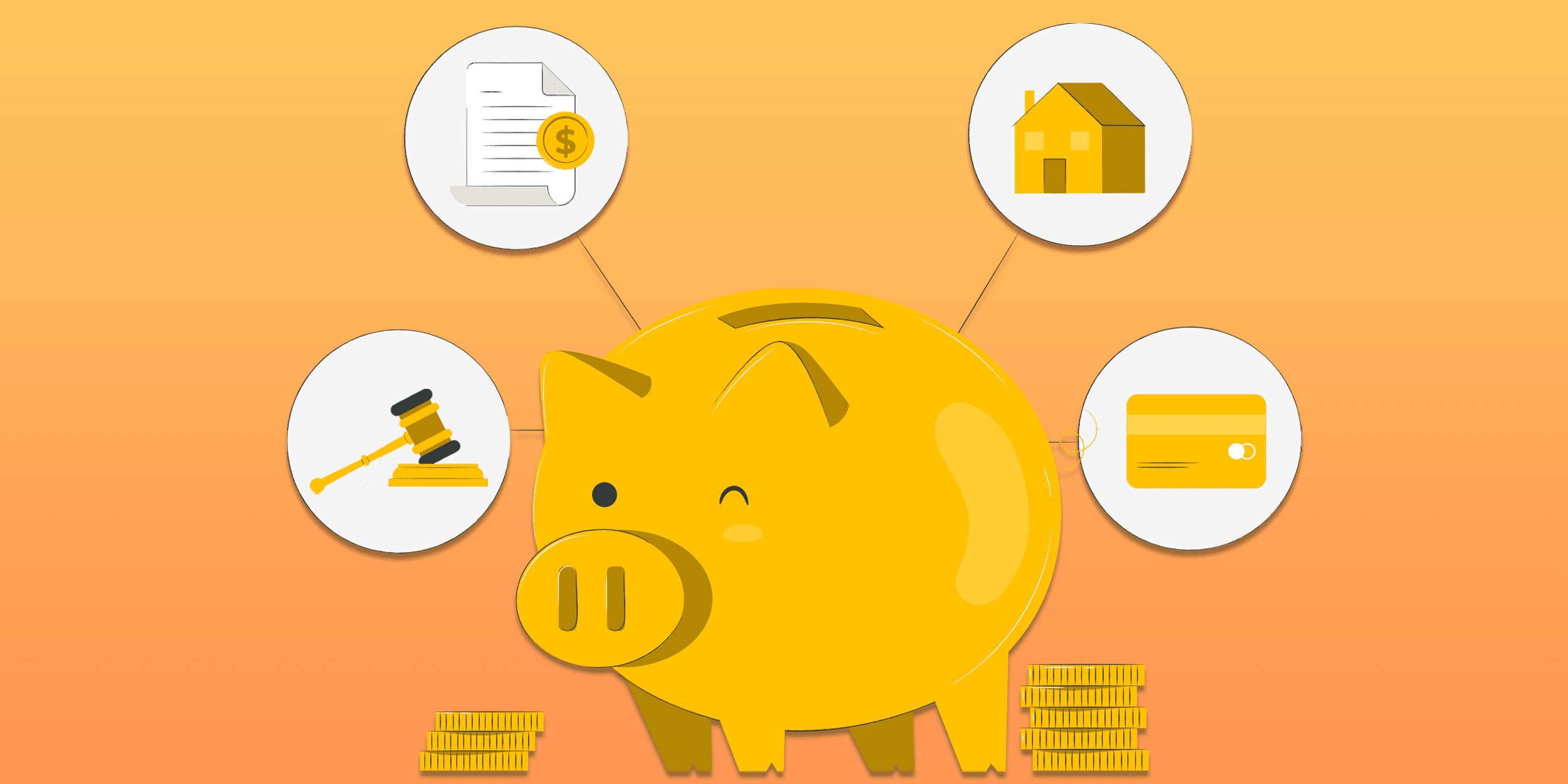

Uncertainty continues to rise in the private lending industry, making it more critical than ever to be certain of the insurance coverage of borrowers as lenders look to protect themselves and their capital. Unfortunately, private lenders, in particular, are far too frequently falling short of what they expect of their customers, with some omitting insurance requirements entirely. This mostly jeopardizes investments if a loss is not adequately insured. Therefore, lenders need to be aware of certain guidelines to implement in the insurance requirements of their transactions.

The asset upon which a loan is taken should be insured at the minimum to the outstanding loan value or higher. Depending on the risk level of the loan, lenders can adopt two coverage levels for insurance: the basic and special forms. The basic form typically covers the risks specified in the insurance with exclusions like theft, damages from water, snow, or ice that could potentially harm the Borrower. On the other hand, the special coverage puts the responsibility of proving that the loss was caused by exclusion on the insurance company; otherwise, coverage is provided.

For instance, as the lender for a real estate investment transaction, you should ensure that you are listed as the mortgage holder on the asset insurance scheme. This is to ensure that you get notified duly before coverage is canceled due to non-payment or other issues arising from the underwriting process. If you receive notice of coverage cancellation for a property you have an interest in, you can compel for coverage with a lender-placed insurance policy.

Understanding the crux of insurance coverage as a lender is critical to the success of lending business. To read more, click here.

About Note Servicing Center

Note Servicing Center provides professional, fully compliant loan servicing for private mortgage investors so they can avoid the aggravation of servicing their own loans and just relax and get paid.

Contact us today for more information.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}